Table of Contents

At its investor day, Twilio promised 21% non-GAAP income by 2027 and $3 billion in free cash flow over the next three years—goals it confidently aims to meet even if it should fall short of revenue targets. And those targets are no less audacious.

The company aims for durable double-digit growth by then and has pledged GAAP profitability moving forward, reporting 11% year-over-year growth for Q4 2024. Overall, Twilio exuded ambition, optimism, and honesty—a charming swagger without the arrogance a dominant player might show.

The three-hour event featured Twilio’s leadership team and customers, spanning over 160 slides. What follows is my ‘The Good, The Interesting, The Unknown’ framework to unpack the content.

The Good

A strong Q4 that ended with 11% growth and, for the first time, GAAP operating profit, served as a preview of earnings to be announced next month. Verify, a non-messaging product, stood out as Twilio’s fastest-growing offering. There was plenty of good news to parade—and all of it hard won.

Just three years ago, Twilio was getting hammered in the stock market for the excesses of pandemic growth. I have a more nuanced take on those years, but it’s true that unprecedented growth triggered equally unprecedented behaviors to keep up. The company has cleaned up the mess and is now focused on capturing market share.

Twilio is framing its growth as a double-digit target, leaning on operational discipline, innovation, and an efficient distribution channel. Partnerships and integrations are key here. The company highlighted its work with Amazon, Google, Snowflake, and OpenAI, in addition to strong relationships with Klaviyo, Braze, and Postscript.

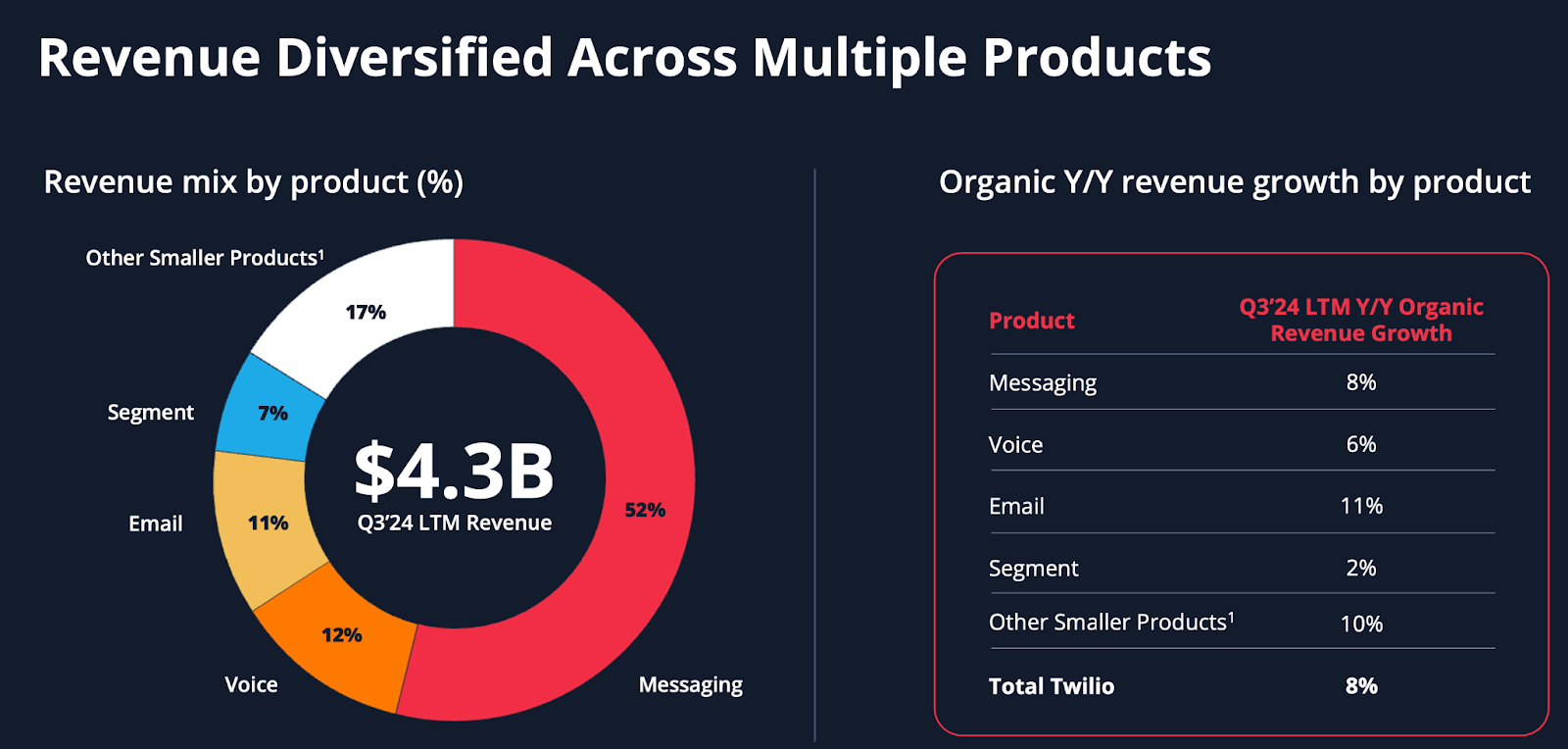

Finally, Twilio’s core CPaaS business remains a moneymaker. Over the last 12 months, it led the industry in both revenues and gross margins, generating $2.2 billion in messaging revenue at 33% gross margins. This also means there’s enough spread in voice and email—both of which have inherently higher margins—for Twilio to sustain its >50% gross margins.

The Interesting

Integrations are central to Twilio’s future strategy, with a focus on working with hyperscalers while doubling down on Segment and AI. The product strategy revolves around a unified consumer profile that enables consent-based communication across channels—a trend that’s quickly becoming table stakes.

Voice and SMS are making a comeback, not just as communication tools but as interfaces for AI-driven interactions. This resurgence adds an incremental $40B to its TAM.

On the growth front, the land-and-expand model was working well with 65% of net new enterprise customers coming from self-signup. This success mirrors Twilio’s international growth, which also has been driven by an opportunistic approach to expansion.

And like Sinch highlighted in its own Investor Day, Twilio is signaling an appetite for “opportunistic” tech and talent tuck-ins—moves that accelerate its growth or enhance its product roadmap.

The Unknown

Let’s unpack the math. 63% of Twilio’s customers purchase only a single product, yet multi-product customers account for 90% of its revenue. Despite this, cross-selling contributes just 7% of revenue—but it’s growing at 17% YoY. This suggests much of that 90% revenue is still concentrated in a single product.

Sure, there are green shoots, but scaling cross-selling in this business is tough. You can’t sell voice, text, and data meaningfully without a forcing function—a product that anchors a compelling use case. The challenge? For a platform as widely used as Twilio’s, the universe of use cases is too broad. Worse, pushing too hard into these use cases risks alienating the ISVs who are ultimately your bread and butter.

The second approach is consultative selling. This requires well-compensated, highly incentivized salespeople who know their customer’s business well and can patiently sell the vision of omnichannel communication. It’s the kind of selling where incentives, teams, and execution must align perfectly to deliver results. And historically, Twilio hasn’t gotten this right.

In 2020, I was a Twilio buyer. I asked my account rep about using Flex because my company was comparing it to Braze at the time. Flex, as I showed him, seemed like a logical next step. But the request was brushed off with a chuckle and, ‘Let’s stick to messaging.’ That exchange said it all—the incentives clearly weren’t aligned.

Fast forward to today, and I’m still not convinced the alignment is there. There’s a communications incentive plan, a CDP incentive plan, and a shared cross-selling incentive plan meant to unify GTM motions.

I’m not saying it won’t work but that the bigger you are, the harder cross-selling gets. Twilio has performed best when it stuck to its product-led roots. A sales-led cross-selling strategy will be a high-risk bet. Perhaps this time, under new leadership, it will be different?

Finally

There’s a lot of jaw-dropping data in the presentation, but none more so than the $158 billion Total Addressable Market (TAM) projected by 2028.

Twilio arrived at this figure by broadening its scope—from CPaaS to CXaaS, which it defines as a combination of CPaaS, CCaaS, and CDP. It’s an ambitious leap, though CXaaS doesn’t exactly roll off the tongue (try saying it fast). If you narrow it down to just communications and data, the TAM stands at $119 billion ($86 billion by 2025).

Now, this talk of TAM would probably annoy my MBA students. Early in the course, I usually tell them to ditch the TAM/SAM/SOM slide—or at least shove it to the back. When you’re building a company and still figuring out product-market fit, TAM is irrelevant. What matters is how well you understand the customer problem.

But when you’re the market leader? TAM matters. Others want to know what you think the TAM is, and so do you.

The communications space is massive, pervasive, and expanding—with plenty of headroom for innovation and for disruption.