Table of Contents

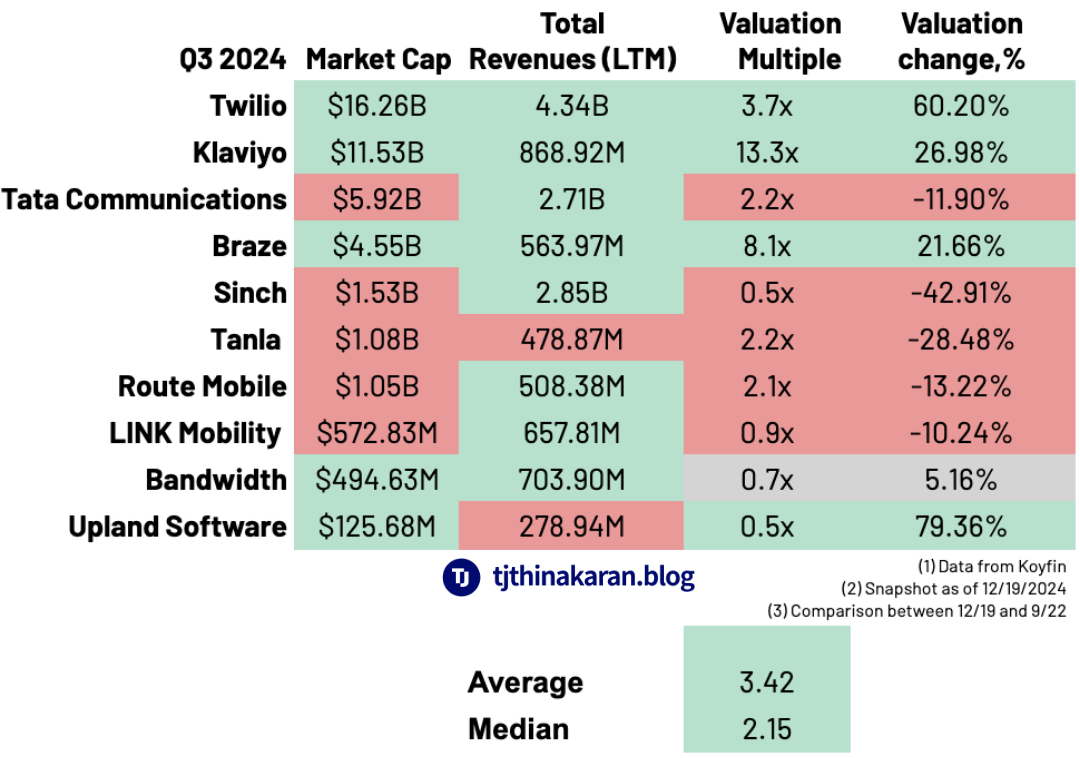

Klaviyo has maintained its position as a stock market darling. Trading at over thirteen times last-twelve-months (LTM) revenue, its $11.53 billion market cap places it squarely in Twilio’s territory ($16.26 billion) despite generating only one-fifth of Twilio’s revenue. Braze also increased its value by 20% to $4.55 billion. When it comes to valuations, not everyone was as fortunate. Sinch, Bandwidth, Tata Communications, Tanla, and Route Mobile all saw their market caps decline. Meanwhile, Upland Software unexpectedly improved its valuation from $70 million to $125 million. The public markets sent a strong signal about the kinds of performance they were rewarding—though the application of that logic feels inconsistent.

Disclaimer: This is not stock advice. Everything about the messaging business interests me, including asset pricing. Use your judgment to invest your money.

Yes, Sinch has had its growth challenges, but it has improved margins and remains the most connected CPaaS provider in the world. Yet it trades at a 50% discount to LTM revenue. Bandwidth achieved double-digit Q3 growth, raised its annual revenue forecast, and improved its opex margin, yet it trades at a 30% discount to LTM revenue.

To put it another way, from September to September, Bandwidth earned $700M in revenues, but as of December 19, the stock market valued it at $494M. For the same period, Sinch earned $2.8 billion in revenues, but the stock market valued it at $1.53 billion. Contrast that with Upland, which earned $278M in revenues but saw its valuation increase from $70M to $125M.

Some may point to the significant debt loads that Sinch and Bandwidth have combined with subpar net-dollar retentions. However, the management of both companies has shown discipline in managing and reducing their debt obligations. But, as mentioned, Mr. Market often misjudges the CPaaS industry and misapplies valuation multipliers. This shouldn’t be surprising. Even Ashwath Damodaran, the dean of valuations, has pointed out the subjectivity and inherent bias in any seemingly rational valuation framework. Perhaps a topic for future discussion.

Yet, the top three on the list—Twilio, Klaviyo, and Braze—showed a trifecta of good growth (i.e., revenue), a money-making product (i.e., healthy gross margins), and efficient go-to-market (i.e., acceptable opex). The rest of the cohort saw valuation cuts between Q2 and Q3 earnings. It’s likely they were missing one or more of the three key factors.

Finally

I use public companies because both the data that the market uses and the judgment of the stock market are plain to see. Private market valuations, by contrast, if not hidden behind NDAs, rely not only on the valuator’s network to gather information but also on their ability to differentiate between meaningless gossip and insightful scuttlebutt. Whether private or public, however, the formula to spot a Taylor Swift remains the same: a great product, a dynamic go-to-market engine, and disciplined, hardworking leadership.