Table of Contents

The last one to release its results, Braze too presented healthy revenue growth—a first-ever non-GAAP profit—and gave some interesting insights into its RCS adoption roadmap. It also showed strong growth momentum and revealed new product-led initiatives.

Disclaimer: This is not stock advice. Everything about the messaging business interests me, including asset pricing. Use your judgment to invest your money.

The Good

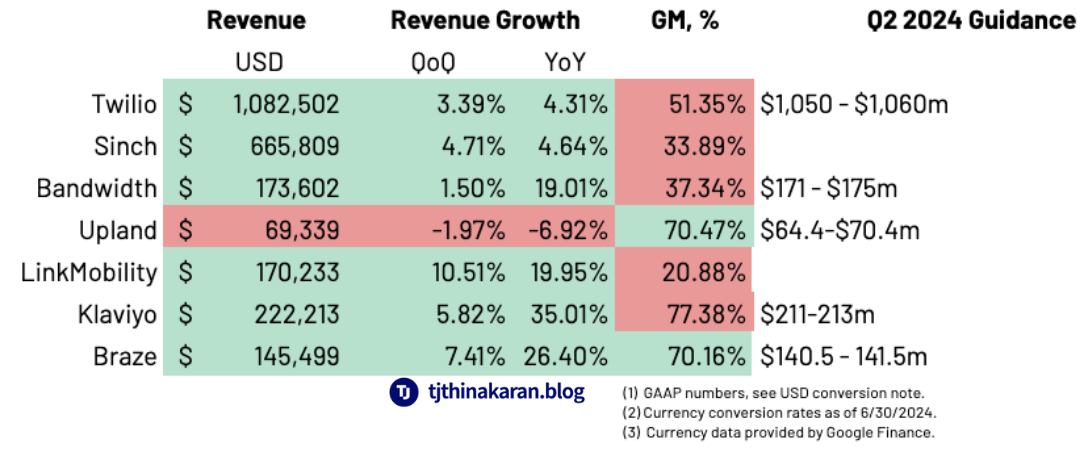

There was a 26% YoY revenue growth, with 96% from subscriptions, plus the first quarter of profitability in both non-GAAP operating and net income. The customer count stands at 2,163, up 10% YoY, with enterprise customers increasing by 28% to 222. New launch partners for the data platform include Telium and Twilio Segment.

Also, a new free trial for startups was announced. But, I wonder (and an analyst pointed out) if fourteen days is too short for a developer trial.

The Interesting

Strong enterprise upsell—61% of revenue is now from enterprise ARR. RCS adoption is boosted by customers’ experiences with WhatsApp and LINE, facilitating a smoother transition to RCS. In fact, they’ve introduced a more flexible credits model, where all credits are available on Braze for RCS usage.

On RCS, CEO Bill Magnuson noted on the earnings call:

“Most of the R&D needs to support things like composition, previewing, testing, and reporting on RCS have already been done in some fashion due to our support of WhatsApp, LINE, or other Braze zone and operated channels like content cards and in product messaging.”

The introduction of the free trial is proof that Braze is relying on product-led growth tools to drive growth. From the earnings call:

“…what you’re seeing in releases like the Braze for Startups as well as broadly the building that we’ve been doing under the product-led growth umbrella, is really looking at the business over the long term…”

The Unknown

Future growth might be a challenge, especially given that in-quarter NRR is marginally lower than the previous quarter. Braze also admits that churn, while expected, is higher than it would like it to be. This begs the question: Is Braze too much enterprise focused? In fact, YoY enterprise revenue as a percentage of the total has gone up from 57% to 61%.

Also unknown is how much of the growth is driven by which channel (email vs. SMS/MMS vs. OTT).

Finally

In a tough business climate, the enterprise is the first to become a hard sell. When the buyer and the user are different people, when the one signing the check is more concerned about costs, optimal product fit takes a back seat. Just ask Slack. Bill and team acknowledge this and, via their free-trial offerings, are trying to get more internal champions to do the selling for them. This brings me to a larger play I see happening.

Building a self-serve flywheel is a demanding task that takes years to perfect. True self-serve platforms that honed their onboarding processes on the SMB long-tail will find it easier to move upmarket. In contrast, enterprise-first players that rely heavily on white-glove instruments like live demos may struggle to penetrate the downmarket.