Table of Contents

Overall, the cohort delivered double-digit revenue growth but with some disclosing single-digit declines; many showed no appetite for M&A, but one is evaluating eleven acquisitions; for this company, RCS drove both revenue and margins while others awaited Apple’s support; for another, political texting drove double-digit growth but this use case barely registered for others; product, partnerships, and new market expansion drive growth across the board; and efficiency remained a priority for all. In the first de-risked year-over-year comparison, the six companies I follow showed varying levels of focus, velocity, and flexibility in pursuing enduring growth.

Disclaimer: This is not stock advice. Everything about the messaging business interests me, including asset pricing. Use your judgment to invest your money.

The Good — Revenue Growth

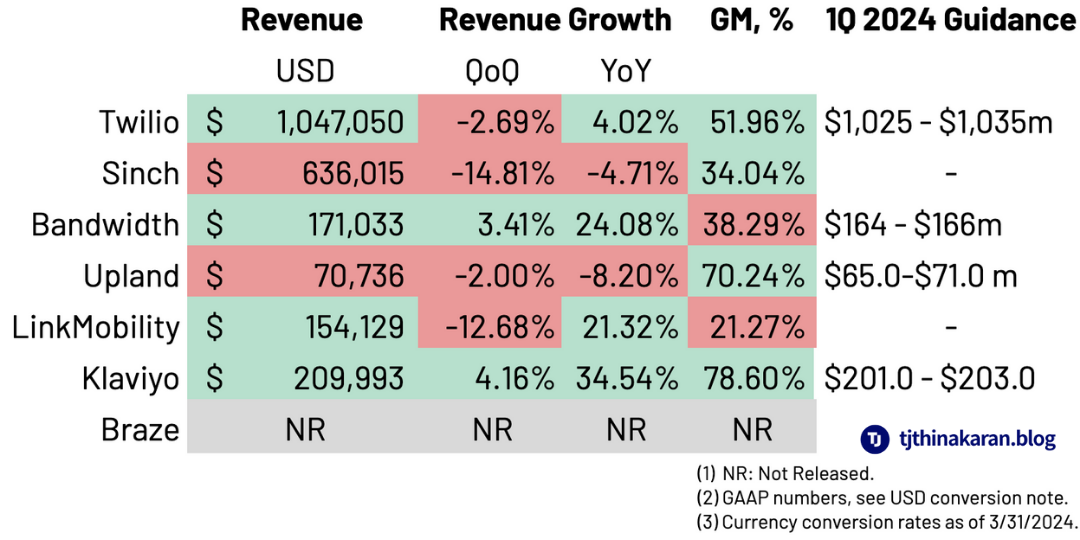

Bandwidth, Klaviyo, LinkMobility, and Twilio all registered double digit growth numbers. Klaviyo led with 34% revenue growth and 78% gross margins. Bandwidth, Twilio, and LinkMobility all beat revenue expectations. Sinch’s revenue decline was a surprise, but the company is showing renewed product focus. And while Upland beat expectations, its extended revenue decline remains an enigma.

- Twilio: The communications business, excluding the Crypto business and the sunsetting of Zipwhip accounts, was up 10% year over year (YoY). Net Dollar Retention (NDR) remained at 105%. The company is also seeing a ‘flex up’ in messaging volumes.

- Bandwidth: Overall revenue grew 24% to $171M with Cloud Communications coming in at $128M. Paper-napkin math shows that if messaging grew 50% to 21% of Cloud Communications, with $3M of that being political messaging (something we’ll talk about later), its messaging business totaled $26.8M for the quarter. Commercial messaging accounted for $23.8M, up from $17.9M last year. Bandwidth expects messaging to hit about $37M in Q2.

- LinkMobility: This quarter saw 20% organic growth, with Net Revenue Retention (NRR) at 110% and revenue churn below 2%. The company processed 4.6 billion messages during the period. Notably, LinkMobility, unlike other companies on the list, reports an increase in traffic from RCS. It is also actively considering 11 targets for potential acquisition.

- Klaviyo: Revenue hit $210M with 35% YoY growth. It continues its aggressive moves into mid-market, stealing from legacy and point-to-point SMS and marketing solutions. In Q1 it found customers to be cost conscious and moving from SMS to email. That however didn’t stop Klaviyo from building international messaging routes. Thus far, Klaviyo exemplifies omnichannel messaging done right.

- Upland: Beat expectations, and had a 8% YoY decline in revenue. It may be looking at M&A as a source of inorganic growth later this year.

- Sinch: Reported a small decline in organic revenue, however it improved gross margins, paid down debt, and reorged the company around a product-led global strategy with a local GTM focus. 80% of the gross profit comes from its Sinch Engage (MessageMedia + MailGun + Old Sinch Engage) and API platform. Some of the revenue pressure came from the voice side of the business (8YY reform effects) as well as walking away from 6 all-you-can-eat deals in EMEA that didn’t fit an acceptable margin profile.

The Interesting — Politics, Partners, and M&A

Politics

SMS and political messaging are huge in the U.S., with estimates suggesting nearly 26 billion political messages this year alone. Bandwidth is aggressively pursuing this market, unlike Twilio and Sinch, who seem wary of the unpredictable revenue and compliance challenges political campaigns pose. These can skew year-over-year comparisons and bring compliance risks—like the backlash from blocking voter outreach as spam. However, Bandwidth has managed these challenges by reporting political revenue separately from its commercial messaging business. This strategy not only mitigates financial volatility but also allows it to capitalize on an earlier-than-expected surge in political messaging this year.

M&A

LinkMobility stands out for its aggressive M&A strategy, currently considering 11 deals. Meanwhile, Sinch is seeking accretive sources of inorganic growth, but only where they align with its product strategy. Twilio and Bandwidth have not made any major statements regarding M&A. Upland, however, may explore potential deals later in the year.

The Unknown — RCS, Partnerships

RCS

I just came from ITW where I had the opportunity to talk about RCS on one of the panels. There’s a lot of fear, uncertainty, and doubt about how RCS will look with the coming Apple support. That is not shared by either LinkMobility, Sinch, or Twilio. In fact, LinkMobility is reaping the rewards of being a major player in the RCS-ready markets of Europe, especially France. As I mentioned in my RCS pricing discussion, France remains one of the shining success stories of RCS adoption. Sinch, for two quarters now, has been touting the impact of RCS. But it, like Twilio, is waiting for the North American rollout. No one, not even the leaders of these powerful corporations, knows how that will play out.

Partnerships

Twilio is using partnerships as a way to drive revenue. This makes sense. It has unique challenges of scale. At a $1B quarterly run-rate, it takes a lot to move the needle. Its partnership with China Unicorn is an early ‘green shoot’ in this strategy. It is also co-selling with Bloomreach. It is clear that Twilio is pursuing a premium-pricing strategy. In any partnership, splitting profits and protecting margins are risks to execution. How Twilio’s long-term partnership strategy unfolds will be interesting to watch.

Finally

A renewed focus on long-term growth, a disdain for incrementalism, and a can-do attitude are apparent from all the calls. The most refreshing aspect has been the near absence of terms like ‘macroeconomic headwinds’ in any of the discussions. These companies feel that their fate is very much in their own hands and that they can continue to grow responsibly. However, the overall chatter from the SaaS industry and the broader industry hasn’t changed much. From HubSpot to Shopify, from former Walmart US CEO Bill Simon to current J.P. Morgan CEO Jamie Dimon, warns that we’re becoming a bit too optimistic a bit too early. With over 30 weeks left in the year, we’ll know who is right soon enough.